UK solar capacity hits 2GW added in 2025, close to surpassing full 2024 total

Solar Media Market Research analyst Josh Cornes tracks the UK’s solar installations from the first half of 2025, with the last six months seeing almost as much installed capacity growth as all of 2024.

The UK has completed over 2GWp in 2025, the best start to the year for 10 years, and is looking to push on with 3.7GWp of utility-scale ground mount solar PV under construction.

At the start of the year, I estimated that between 3GW and 3.5GWp would be added to the UK market in 2025. With the completion of Cleve Hill, and residential rooftop being stronger than originally expected, the UK has surged past 2GWp already.

Ground mount continues to make up over 70% of the capacity, with over 1.5GWp completed. This is boosted massively by the first solar nationally significant infrastructure project (NSIP) Cleve Hill (373MW) being completed. This is as well as 14 other sites 50MWp or above also completed, making up over 60% of the added capacity, with Low Carbon and NextEnergy recently energizing over 400MWp between them.

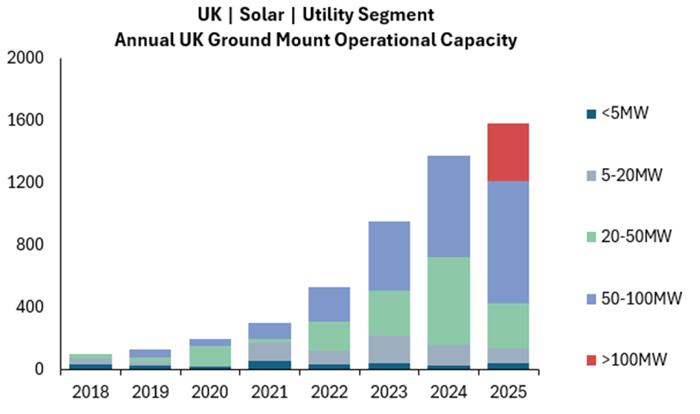

Figure 1: Annual UK ground mount operational capacity broken down by capacity sizes, outlining the push and need for large scale solar.

As we can see from Figure 1, populated with data from Solar Media Market Research, large scale solar (>50MWp) is dominating the market, making up not far off 70% of the capacity that’s been built in 2025, a trend that’s been increasing year on year (YoY) since 2018.

With a further 1GW that started construction over a year ago and standard build out times being anywhere between 30-60 weeks, there’s potential for ground mount to complete over double the amount seen in 2024.

Commercial rooftop, as expected, has remained steady, off to a great start being ~20% up YoY.

With the government backing residential rooftop with big incentives such as the new build mandate detailed here, continued backing has definitely had a big impact on rooftop as a whole, with new announcements of a further £10m being assigned, detailed here.

Utility scale solar submissions increase

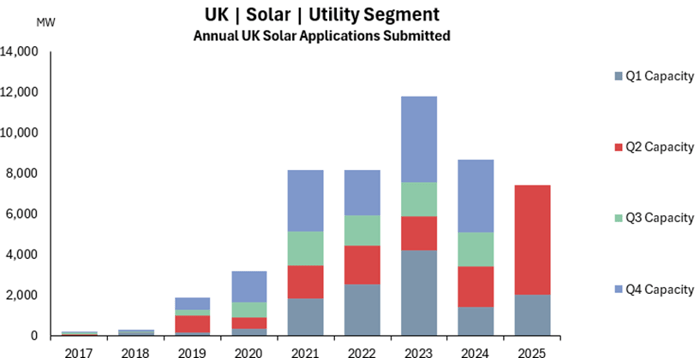

Submissions for utility scale solar farms has been at heights not seen before. With over 7GWp submitted to date this year and over 5GW submitted in Q2, this was the best first half of the year in history, with Q2 being the best quarter for submissions.

Figure 2: Solar submissions continue to Rise in 2025, with Q2 having the highest capacity submitted in history.

As expected, this is largely driven by government-level projects with over 3GW being submitted to their relevant governments in the last 3 months. A total 12 projects with combined capacity of 6.6GWp have been submitted to the Planning Inspectorate since the Labour government took over.

It’s hard, however, to tell if the uptick in solar NSIPs entering the planning system since the election is as a result of improved developer confidence following Miliband’s quick development consent order (DCO) approvals and supportive signals from government, or the Clean Power 2030 plan pushing them to act sooner rather than later.

Submissions at local planning authority (LPA) level are also strong, having had over 3GWp submitted in H1, however this is only going to lead to more strain on decision wait times.

Although submissions have been at an all time high, with developers submitting their gate 2 applications for grid connections, the majority will have got their projects into planning already. Therefore, the next three months are expected to be quiet giving LPAs an opportunity to catch up on the existing 8GWp that they’ve yet to approve.

Refusals are something else that need to be looked at, with 14 projects, a total of over 750MW, having been refused in 2025. With almost 90 projects totalling almost 2.6GW having been approved at LPA level, over 20% of the capacity that’s been decided this year has been refused.

Refusals are also seen at the appeal stage. Although the year started with all of the first 14 LPA refusals being approved at appeal, 3 of the last 6 projects taken to appeal have now been refused, with Wood Lodge Solar Farm in Northamptonshire being the latest refusal. With 24 projects (1.3GW) currently at appeal and a further 20 (1GW) likely to lodge an appeal, let’s hope this trend doesn’t continue.

The UK has surpassed 22GWp of operational capacity, with almost 14GW coming from ground mount alone. 2025 is setting records with planning submissions, at both LPA and Government level. Backing from the Labour government is starting to point Solar in the right direction but there are bumps in the road that need ironing out, with planning being slow, grid being a large issue and resources when it comes to building out this large pipeline being an elephant in the room.

All the data above is taken from Solar Media Market Research’s analysis, which can be accessed here.

ORIGINAL ARTICLE: SOLAR POWER PORTAL